Flowmeters: 20-year data show a shift to three technologies

Key Highlights

- Sales volume shifted from low-cost traditional meters toward higher-value advanced meters like Coriolis, magnetic, and ultrasonic.

- Rising oil and gas prices and the need for accurate measurement of valuable fluids will further strengthen demand for advanced flowmeter technologies.

In February, March, and April 2001, I published three articles in Control on new technology and traditional technology flowmeters. The purpose of these articles was to define new technology flowmeters and traditional technology flowmeters, and to view the flowmeter market in light of this distinction. In the February 2001 article, I wrote:

“One of the most interesting developments in the flowmeter market today is the battle between newer technologies and traditional flowmeters. New technologies include Coriolis, magnetic, ultrasonic and vortex flowmeters. Traditional technologies include differential pressure (DP), turbine and positive displacement (PD) meters. While there is a general trend towards new technologies and away from traditional meters, this change varies greatly by industry and application.”

I reiterated this shift towards new technology flowmeters in the second article in March 2001:

“Much has been written in the past five years about the superiority of new technology flowmeters over traditional technology meters. There is no doubt that there is a fundamental shift in the market towards newer technologies, notably ultrasonic and Coriolis, and away from more traditional flowmeters. But these shifts often take many years to complete, and awareness that a shift is occurring may present opportunities to traditional technology suppliers. Even if the flowmeter market is flat, customers as a group will spend as much on that type of flowmeter this year as they did the preceding year. If some suppliers are reducing their research investments in traditional-technology flowmeters, it may present an opportunity for other suppliers of those same technologies.”

While I initially included thermal flowmeters among the traditional meters, extensive discussions over the course of a year with Dr. John Olin of Sierra Instruments later convinced me to classify them as new technology meters.

In 2003, Flow Research published our first Volume X, a market research study on all 10 of the main flowmeter technologies. By researching each technology individually, we were able to size the flowmeter market in 2002 in terms of each flowmeter type in both dollars and units. We also included five-year forecasts. Since that time, we have done eight more editions of Volume X, publishing the 9th Edition in 2024. We are currently working on the 10th edition.

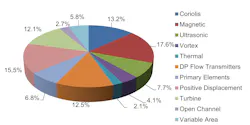

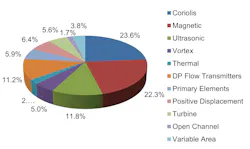

The following two pie charts show how the flowmeter market has changed from 2002 to 2022.

These charts reveal quite a lot about how the worldwide flowmeter market has changed in the 20-year period from 2002 to 2022. Coriolis flowmeters are the biggest winners in terms of revenues, increasing their share of the total market from 13.2% in 2002 to 23.6% in 2022.

Magnetic flowmeters also increased their market share from 17.6% in 2002 to 22.3% in 2022. Ultrasonic flowmeters showed a share increase from 7.7% in 2002 to 11.8% of revenues in 2022. Combined, Coriolis, magnetic and ultrasonic flowmeters increased their share of the total flowmeter market from 38.5% in 2002 to 57.7% in 2022. This makes for a remarkable shift in the flowmeter market during this period.

As predicted in early 2001, there has been a dramatic shift in the flowmeter market from traditional (conventional) flowmeters to new technology flowmeters. This is not a matter of speculation; the data shows that it has already occurred. These technologies accounted for nearly 60% of the market in 2022, up from less than 40% of the market in 2002.

Get your subscription to Control's tri-weekly newsletter.

What is behind this dramatic shift in flowmeter technology? The flowmeter market has shifted from mechanical measurement technologies toward electronic, digital and higher-accuracy systems. In 2002, positive displacement and turbine flowmeters accounted for 27.6% of worldwide flowmeter revenues. In 2022, those two technologies accounted for just 12% of worldwide flowmeter revenues. This change represents a shift from mechanical, inferential, and lower-coupling technologies to direct measuring, electromagnetic, and digital/acoustic technologies. This change was driven by the need for premium applications such as LNG and custody transfer, multipath and multiphase systems, and higher prices per unit.

The relatively small drop in market share for differential pressure (DP) flow transmitters and primary elements reflects their installed base advantage. It also reflects significant improvements in DP flow transmitters, including greater precision and accuracy, the development of multivariable pressure transmitters and the trend towards integrating primary elements with DP flow transmitters. Another trend is improvements in primary elements, including combining multiple technologies into one. Examples include the Accelabar and the VorCone.

The shift in units sold over the 20-year period tells a similar story. The largest number of flowmeter units sold in 2022 were magnetic flowmeters, DP flow transmitters and variable area meters. Positive displacement and turbine flowmeters, along with primary elements, showed a decline in the number of units sold from 2002 to 2022. At the same time, the number of Coriolis, ultrasonic and magnetic flowmeters sold in 2022 compared to 2002 increased dramatically. The flowmeter market has shifted away from low-cost volume meters to high-value, high-performance flowmeters.

Flow Research gathered the data distilled in this article over the course of 20 years, although we have data on the worldwide flowmeter market beginning in 1993. Our approach has been to do a market study on each flowmeter technology individually, then assemble this data into a picture of the entire market in a publication called Volume X. This is a bottom-up method of research. Using this method, we have assembled data for 2002 and for each intervening year through to 2022. The data presented in the 9th edition is the result of thousands of hours of research over the years, but it is only a tiny fraction of the data we have available.

We are currently working on the 10th edition. From what we have seen so far, the trends outlined in this article are continuing. Coriolis, magnetic, and ultrasonic flowmeters have come to dominate the flowmeter market, as end-users opt for high-value and high-performance solutions. And with both oil and natural gas prices at record highs, the need to accurately measure these high-value products will increase dramatically. High oil and natural gas prices are likely to increase the dominance of Coriolis, magnetic and ultrasonic flowmeters in the flowmeter market.

Flow Research has started a Wordflow Knowledge Base to track these changes and to explore the flowmeter market from multiple points of view. This site contains nearly 300 published articles and examines many flow technologies in depth. These are only some of the fascinating discussions we have engaged in while studying the market for more than 30 years.

About the Author

Jesse Yoder

Columnist

Jesse Yoder is founder and president of Flow Research Inc., which conducts market research studies in a wide variety of areas, including the flowmeter market.

Leaders relevant to this article: