Ins and outs of remote I/O deployment

OUR WORK with Venture Development Corp. (VDC) from time to time encourages readers of Industrial Networking to participate in relevant market studies these analysts conduct. That lets us share, first hand, the findings that most impact your applications, be it right now or in the future. It’s also a good way to get your collective thoughts about a technology area in front of the appropriate members of the vendor community.

|

For a look at some of the findings from our Fall ’06

|

This time, we’ll summarize data from the Remote I/O study update VDC published mid-2006 that indicates the market segments which have the strongest growth in use of remote I/O. We’ll also summarize the control buses and networks that currently enjoy favor in remote I/O applications, and how that looks going into the future. The study includes the responses of end users in the discrete manufacturing and processing plant segments, industrial machine builders, and system integrators. Respondents specified whether they used traditional DCSs, PC-based control, or PLCs as their control platform.

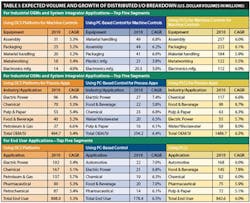

DCS Users

Petroleum & gas (6.6% CAGR to $37.5M), water/wastewater (5.5% to $20M), and electric power generation (5.4% to $96M, the biggest market segment) project the best remote I/O growth into 2010 for OEM and SI applications in the process industries. Chemical is the second largest market segment here at $70M.

For end users of DCS systems, applications in petroleum & gas (5.7% to $137M) and food & beverage (5.6% to $67M) project the fastest growth. Electric power is the largest 2010 market segment at $192M, followed by chemical at $167M.

PC-Based Systems

For OEM/SI PC system applications totaling at least $1M in the process industries, electric power generation (7.4% to $27M, the largest segment) and petroleum & gas (7% to $13M) lead the way. Food & beverage checks in as the second largest segment in this grouping at $22M

For end users of PC-based systems, applications for remote I/O are projected to grow the fastest in plastics ($7.1% to $15M) and automotive (7% to 22M). Automotive is the biggest projected 2010 segment, while electric power is next at $21M

Those PLC Users

For OEM/SI PLC-based projects in process industries, petroleum & gas should show the fastest growth (10% to $19M) with food & beverage second (8.7% to $99M, the second largest volume). Chemical has the biggest volume in this grouping at $117M.

For end users of PLC solutions, consumer products manufacturing will see the biggest growth rates for remote I/O (8.4% to $59M), followed by food & beverage at 7.8% to $145 M, the second largest segment in this grouping. Automotive leads the remote I/O consumption in this grouping with $168M.

Table I below summarizes all these market segment leaders in remote I/O use.

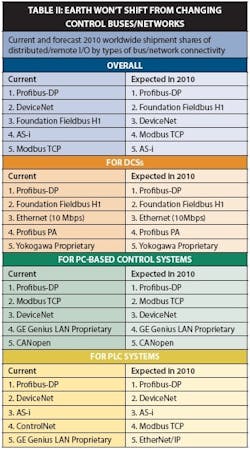

Bus Choices for Remote I/O

In the DCS grouping, Profibus-DP holds nearly 20% of the market, followed by Foundation fieldbus H1 at nearly 19%.

For PC-based systems, the remote I/O is part of a Profibus-DP network at an almost 30% market share. Modbus TCP was next at just under 13%. In PLC systems, Profibus-DP claims 39%, followed by DeviceNet at 8%.

Table II below provides more relevant data.

Price Drops Expected

Considering these to be relative average prices (not trying to compare feature and spec subsets) , DCS remote analog I/O should decline about $48.75 compared with a $52.57 2005 baseline, or about 7.3% by 2010. The expected change is similar for analog I/O in the PLC-based segment, with a 6.3% decrease to about $48.55 projected. Price decreases in analog I/O for PC-based systems should fall a similar 6.3% to $40.36.

Declines in the price of digital I/O follow suit. Digital I/O for DCS systems is expected to drop 7% to about $9.30, while digital I/O for PLC systems should fall 7% to about $8.77, and PC-based digital I/O drops almost 6.5% to 7.59.

The study data confirms that the price of a digital I/O point is about 15-20% of the price of an analog I/O point for a common IP20 non-block module.

The inclusion of a bus/network interface typically will raise the price of a block I/O point about 50%. In addition, a unit with a higher environmental rating such as IP67 is likely to be 20-25% more costly.

Maintenance Issues

Figure 1 identifies a laundry list of requests that define some of the detail of simplification, but the message is give users the means to identify and solve problems themselves.

For a look at some of the findings from our Fall ’06 article on remote I/O, visit Remoteio.

The study respondents made known their ideas on how suppliers can make remote I/O simpler and reduce the maintenance of the devices. Providing self-diagnostics capabilities and easier to use diagnostic tools were the clearly the two top answers given.Comparing the last base year of this study for average price per I/O point against expected costs by 2010, shows an expected price decrease. Parsing the worldwide total of remote I/O volume by bus/network type shows that Profibus-DP will hold 31% of this market by 2010. DeviceNet and Foundation fieldbus each will hold 7% of the market at that time to claim the second and third spots. Modbus largely holds its own through 2010, while most of the dramatic growth comes from Ethernet/IP replacing DeviceNet and ControlNet, and the steady growth of other Ethernet hybrids in the PC-based and PLC-based groupings.For OEM/SI equipment applications in the PLC systems segment, textile manufacturing equipment will show the fastest remote I/O growth (8.5% to $17M), followed by heat-treating equipment (7.7% to 9.5M). These clearly are small segments. The largest in this grouping is assembly equipment at $260M, followed by packaging equipment at $222M.For OEM and SI PC-based equipment applications, textile manufacturing equipment again shows the fastest remote I/O growth at nearly 11%. This market is larger than the DCS segment, with 2010 volume pegged at $8M. Material handling equipment comes second with a 6.8% projected annual growth to $49M, which is the biggest PC-based application segment. Assembly equipment is predicted to be the second largest at nearly $44M.For OEM and SI equipment applications in DCS-user segments, the fastest growth in remote I/O consumption is in textile manufacturing equipment, with a projected average annual growth rate approaching 10%. It’s also one of the smallest market segments for remote I/O, with 2010 spending expected only to be about $1.6 million. Compare this with growth rates of 5.4% for assembly equipment and metalworking equipment in markets, which in 2010 should reach $31 million and $18 million. Assembly equipment represents the biggest market segment by 2010, with packaging equipment next at $25M .